What is the Self prepared P&L?

Self Prepared P&L is a good choice for self-employed borrowers who can not be qualified with agency loan and do not want to provide varities of income documents.

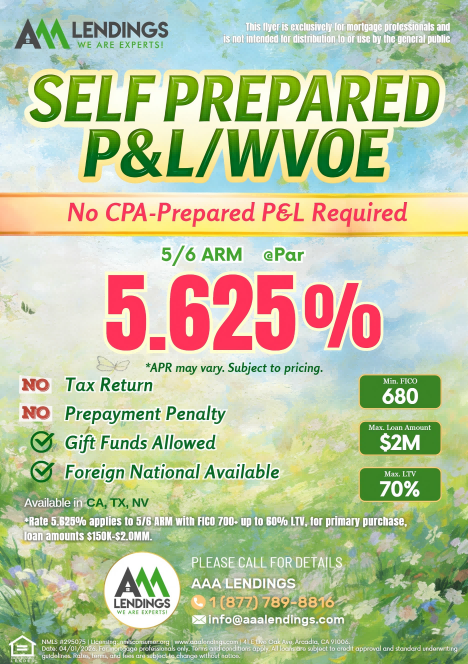

Self Prepared P&L Program Highlights

|

Max. LTV 70% |

|

|

5/6 ARM, 7/6 ARM

♦ Foreign National Available

♦ Gift Funds Allowed

♦ No CPA-Prepared P&L Required

♦ No Tax Return Needed

♦ No Prepaid Penalty

Available in CA, NV, TX.

What is P&L? Who can apply for P&L?

P&L stands for Profit & Loss. Under this program, eligible self-employed borrowers may use a self-prepared P&L or CPA-prepared P&L to document income, subject to guideline requirements.

For this program:

- Salary borrowers with ownership under 25% may be documented with WVOE (FNMA Form 1005) and verbal verification of employment.

- Self-employed borrowers with ownership of 25% or more may use self-prepared P&L or CPA-prepared P&L.

Self Prepared P&L Fast Approval Requirements

When submitting a loan, the following may be required:

- Two years of current business license

- For applications received on or before 6/30: YTD Profit & Loss Statement plus one full year Profit & Loss Statement

- For applications received on or after 7/1: Current YTD Profit & Loss Statement

- CPA letter from the CPA who prepared the previous two years’ tax returns, verifying business ownership, same business location for at least two years, and two years in business

If you have any questions about Self prepared P&L program,

Please email to hello@aaalendings.com or call us: 1 (877) 789-8816