Why did GDP beat expectations?

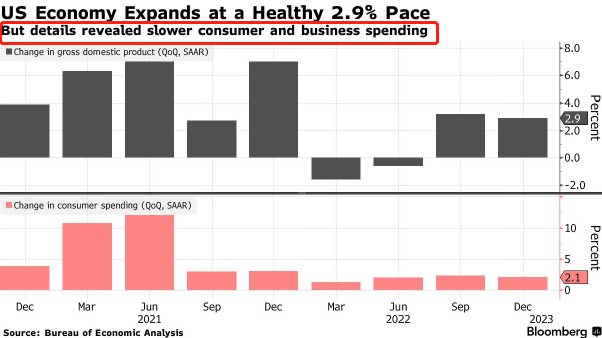

Last Thursday, Commerce Department data showed that U.S. real GDP grew at a 2.9% quarter-over-quarter rate last year, slower than the 3.2% increase in the third quarter but higher than the market's previous forecast of 2.6%.

In other words: while the market assumed that economic growth would take a severe hit in 2022 from the Fed’s hefty rate hike, this GDP proves it: economic growth is slowing, but it is not as strong as the market had expected.

But is this really the case? Is economic growth still very strong?

Let's take a look at what exactly is driving the growth of the economy.

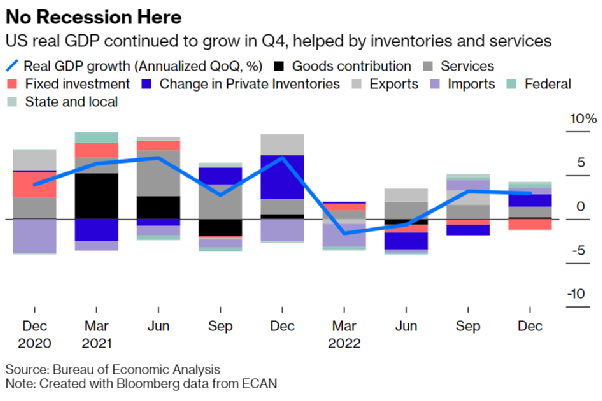

Image source: Bureau of Economic Analysis

In structural terms, fixed investment has fallen by 1.2% and have been the biggest drag on economic growth.

Since the Fed’s rate hike has driven up borrowing costs, it stands to reason that fixed investment would decline.

Private inventories, on the other hand, were the main driver of economic growth in the fourth quarter, rising 1.46% from the previous quarter, reversing the downward trend of the previous three quarters.

This means that companies are starting to replenish their inventories for the new year, so growth in this category was erratic.

Another set of data caught the market's attention: personal consumption expenditures rose by only 2.1% in the fourth quarter, well below market expectations of 2.9%.

Image source: Bloomberg

As the main driver of economic growth, consumption is the largest category of U.S. GDP (about 68%).

The slowdown in personal consumption expenditures suggests that purchasing power is very weak at the end and that consumers lack confidence in future economic prospects and are unwilling to spend their own savings.

In addition, domestic demand (excluding inventories, government spending and trade) grew by only 0.2%, a significant slowdown from 1.1% in the third quarter and the smallest increase since the second quarter of 2020.

The slowdown in domestic demand and consumption, is the most obvious harbingers of a cooling economy.

Sam Bullard, senior economist at Wells Fargo Securities, agrees that this GDP report could be the last really positive, strong quarterly data we'll see for a while.

The Fed's "dream come true"?

Powell has repeatedly stated that a soft economic landing is “possible.”

A "soft landing" means the Fed keeps high inflation under control while the economy shows no signs of recession.

While the GDP numbers are better than expected, it must be admitted: The economy is slowing.

One could also argue that an economy in recession is hard to avoid, and that the GDP beat simply means that future recessions could come later or on a smaller scale.

Second, signs of recession in the economy have affected employment.

The number of initial claims for U.S. unemployment benefits fell to a nine-month low in January, but at the same time the number of people continuing to receive U.S. unemployment benefits began to rise again.

This means that fewer people are newly unemployed, but more people are not finding work.

In addition, the sharp decline in retail sales and factory output over the past two months is evidence that the economy is on another downward spiral - the economy is still on the road to recession, and the dream of a “soft landing” may be hard to achieve.

Some economists believe that the U.S. is more likely to experience a “rolling recession”: a sequential decline in economic activity in various industries, rather than a one-time slump.

Interest rate cut expected soon!

The Personal Consumption Expenditures (PCE) price index, an inflation indicator of great interest to the Federal Reserve, rose 3.2% in the fourth quarter from a year earlier, the slowest growth rate since 2020.

Meanwhile, the University of Michigan’s 1-year inflation expectations continued to decline in January, falling to 3.9%.

Core inflation has improved significantly, which greatly reduces pressure on the Federal Reserve - further rate hikes may not be necessary and more attention can be paid to economic growth.

Based on GDP, on the one hand we see a gradual slowdown in economic growth, and on the other hand, due to emerging recession expectations, the Fed will only raise interest rates moderately in the first half of the year in order to achieve the softest possible landing for the economy.

On the other hand, this may be the last quarter of solid GDP growth, and if the economy deteriorates in the second half of the year, the Fed may have to move to easing before the end of the year, and a rate cut is expected soon.

Economists also say that because of technological advances and the transparency of Fed policy, the lagged effect of rate hikes is less than in the past, causing financial markets to anticipate prices in response to market expectations.

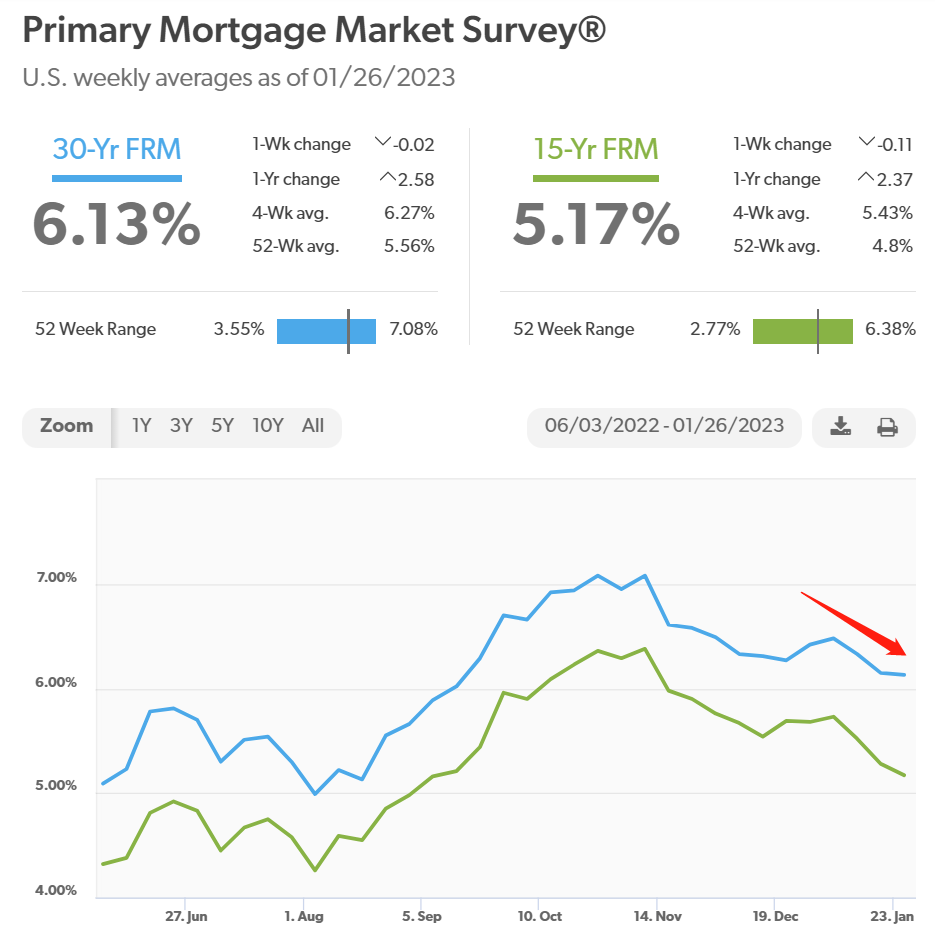

Image resource: Freddie Mac

As the Fed slows the pace of rate hikes, mortgage rates have trended lower, and new home sakes rose for the third month in a row in December, suggesting that the housing market may be starting to recover.

If an interest rate cut is expected, the market will also anticipate prices, and mortgage rates will then fall more quickly.

Articles Sharing:

Will Powell become the second Volcker?

When Record-high Home Prices Meet Crazy Interest Rate Hikes

Statement:

This article was edited and compiled by AAA LENDINGS, the copyright belongs to AAA LENDINGS website, it doesn't represent the position of this website, and is not allowed to be reprinted without permission.

阅读原文 阅读 1387