Is this the last "carnival"?

Recently, sounds such as the "collapse", "bubble burst", and "housing prices are going to fall" continue to appear, which cause a lot of panic.

So, what is the real situation of the housing market? Whether the last "carnival" is approaching? Let's look at some data.

Data from: Redfin.com

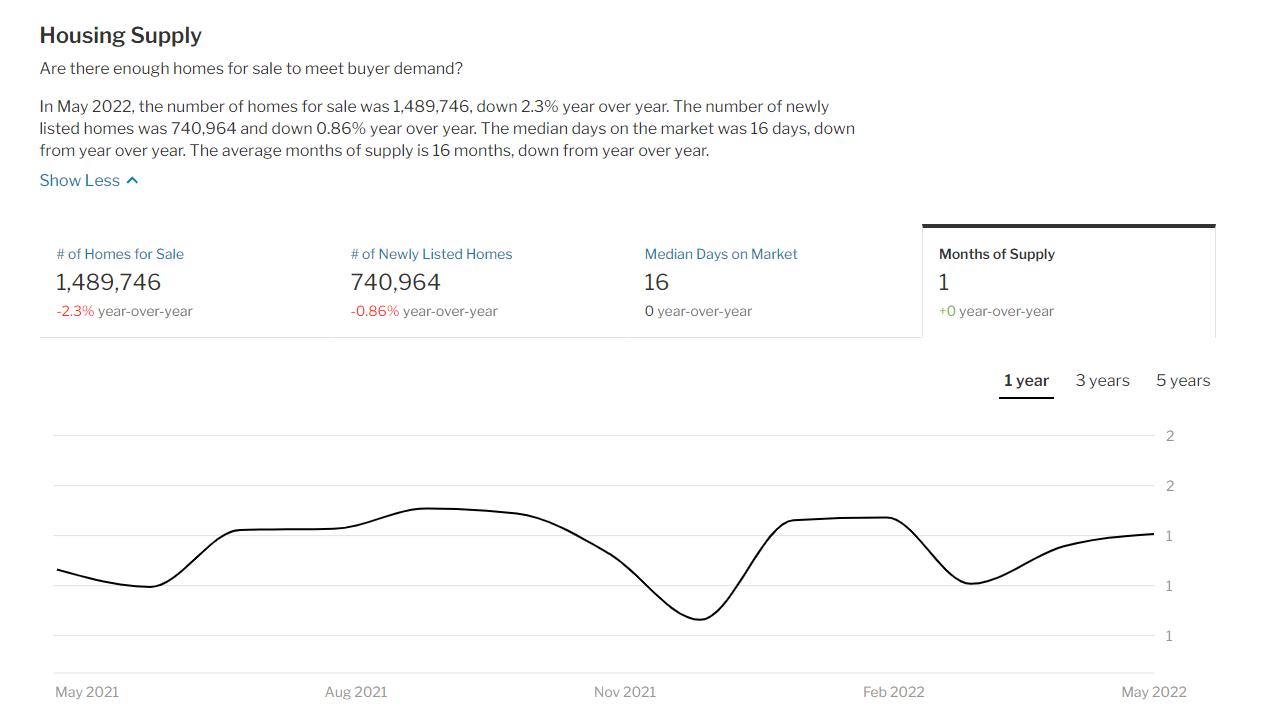

At the end of May, there were 1.48 million unsold homes in inventories, which are equal to one month's worth of sales, and the housing market is still in “short supply”.

While housing starts were weaker than was expected in May, decreasing 14.4 percent to 154,900 units, which is the slowest pace of starts since April 2021, according to the data from the Census Bureau on May 16.

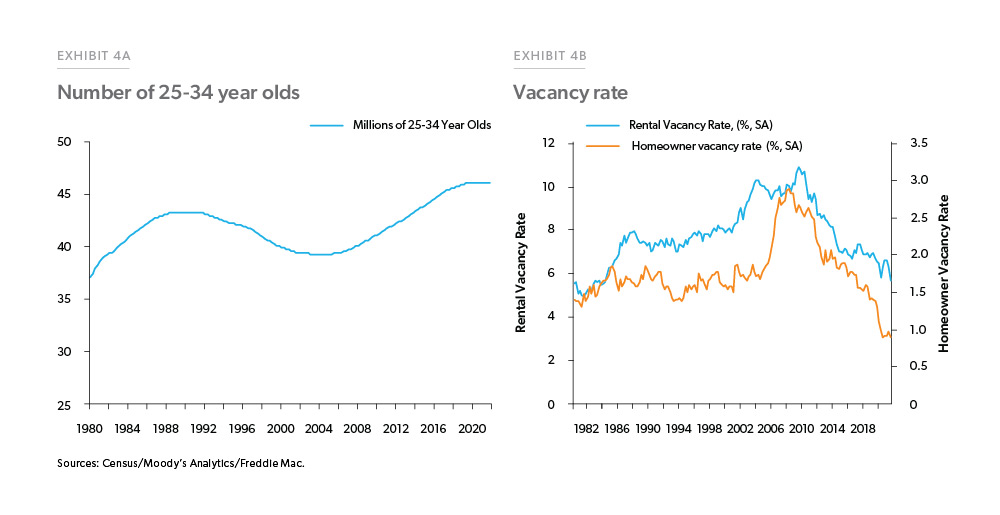

Data from: Freddie Mac

Besides, there are now 18 percent more 25- to 34-year-olds people nationwide than in 2006, meaning that there are 6.6 million more potential first-time homebuyers. However, this population growth of potential homeowners is not matched by enough new homes.

This suggests that strong demand from first-time homebuyers will continue in the foreseeable future.

All of the above data suggest that the inventories of new and existing homes remain at a low point compared to the total housing stock; the housing vacancy rates are at historic lows. Still, the speed of household formation is far outpacing housing starts, and the supply and demand imbalance in the housing market will continue for quite some time.

Supply-side dynamics support the housing market, and the housing scarcity will underpin home prices, making a housing market crash virtually impossible.

Interest rates surge, will the property market cool?

As interest rate hikes continue to ramp up, mortgage rates are soaring, topping 5.8 percent as of Thursday (Freddie Mac).

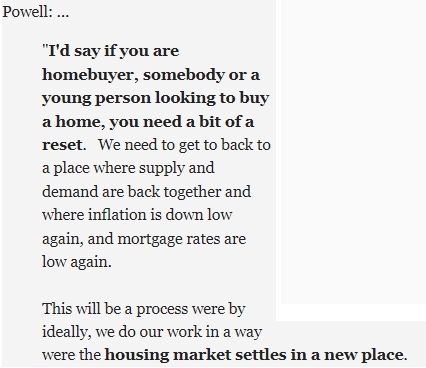

After the rate hike, Powell also said at the press conference that as interest rates rise, the current housing market is also changing.

However, in response to the current state of housing market supply and demand, Powell said that even with rising interest rates, prices are likely to keep rising for some time.

Rising mortgage rates have put many homebuyers on the sidelines, leading to a slowdown in property sales.

Home sales declined for the fourth consecutive month in May, according to a report released on Tuesday. Although the number of property deals continues to fall, prices have hit new highs.

But these data in May include deals completed before the 75 basis point rate hike this month. It is estimated that the contract was signed in March or April.

This indicates that the impact of rising mortgage rates has not been fully reflected from the data, home sales are expected to fall further in the next few months.

Powell said that ideally our work will stabilize the housing market at a new position, with housing supply and credit availability at appropriate levels.

The Freddie Mac study estimates that for every 1 percentage point increase in interest rates, price growth will slow by 4 to 6 percentage points and home sales will slow by about 5 percent.

While higher short-term interest rates contribute to the cooling of the housing market, they also benefit to rebalance housing supply and demand and gradually stabilize the market in a“new position”.

The moon will not be clear until the clouds open

The housing market is indeed cooling down, as evidenced by the decrease in the number of housing deals and in the percentage of price increases as well as the increase of the time for new homes to come on the market.

The regulation of the real estate market by the Fed’s interest rate increase can be said to be immediate and very significant.

But generally speaking, the impact of rising interest rates on the real estate market can be divided into two results: a group of buyers will rush to lock in the deals before interest rates rise further, resulting in the reduction of housing inventories in the market.

After interest rates have already begun to rise in the second phase, the market cools as more buyers choose to wait and see as borrowing costs increase and uncertainties about the future grow.

However, with increased inventories and reduced bidding, the cooling of the housing market is more of an opportunity for new buyers.

Data from: Fannie mae

Besides, according to Fannie Mae’s forecast, mortgage rates are likely to fluctuate slightly over the next two years, but will remain at around 5%.

The era of low interest rates has come to an end, and the market will gradually get used to the “healthy” rates.

The rising tide will lift all boats, but when the flood subsides, it is easier to seize the real “good time” by going against the tide.

Articles Sharing:

![]() Will Powell become the second Volcker?

Will Powell become the second Volcker?

Statement:

This article was edited and compiled by AAA LENDINGS, the copyright belongs to AAA LENDINGS website, it doesn't represent the position of this website, and is not allowed to be reprinted without permission.

阅读原文 阅读 2048